Awin’s 10 trends from Cyber Weekend 2023

Written by Alfie Staples on 12 minute read

We dive into the shopping data from a busy Cyber period to reveal some of the key insights and trends that emerged over Black Friday and the wider Q4 peak.

Doubts were cast over this year’s Cyber period amidst the ongoing economic squeeze that’s impacting consumers across the globe. With many shoppers shifting their priorities to adapt to the circumstances, many experts questioned how successful the key shopping period would be in 2023.

Awin’s insight experts shed light on how the online sales extravaganza performed from an affiliate perspective.

1. Shopper confidence varies between the US and Europe

Despite concerns around spending from advertisers and marketers across the Cyber period, ecommerce sales outperformed expectations. In the United States especially, ecommerce performance was up 8.5% compared to last year according to Mastercard.

Awin saw a similar trend on the network - US revenue was up by 7.4% on Black Friday, bolstered by a 15% increase in AOVs as consumers spent almost $15 more per transaction compared to 2022.

Multiple key sectors saw significant increases in AOVs, helping to boost overall revenue on Black Friday.

- Clothing +6.4%

- Computers +8.1%

- Home & Garden +7.4%

- Health & Beauty +6.4%.

By contrast, European consumers appeared more hesitant. Sales on Black Friday itself were down by 2% annually. However, sales across the entire Cyber Weekend were up 3.3% compared to 2022 and revenue followed suit with a 6% increase. Europe’s shoppers also spent around €2.33 more per transaction compared to last year.

Looking at individual sectors, European shoppers displayed similar priorities to their US counterparts – Home & Garden saw some of the sharpest uplifts compared to 2022 with a 21.3% increase in AOVs, while Clothing increased by 14.8%, over €10 more per transaction.

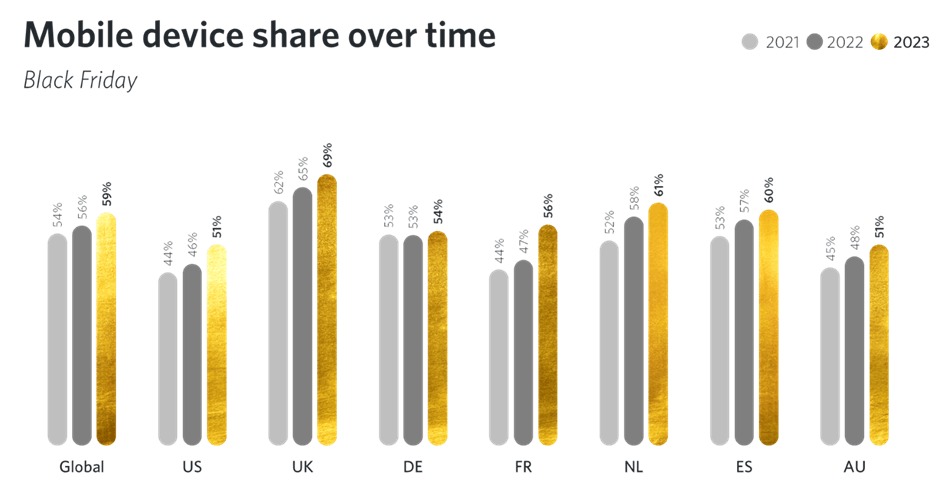

2. Black Friday 2023: The year of mobile transactions

Device activity during Cyber has been upwardly mobile for some time. It was only a matter of time before it became the device of choice for shoppers. The share of sales derived from mobile devices across Awin’s network had already passed the 50% threshold in 2022. But this year saw every individual market pass that threshold for the very first time.

Whilst market leaders like the UK and Netherlands further cemented their status as mobile-first markets for online shopping, we saw markets like the US, and especially France, also reach this tipping point for the first time in 2023.

Looking from a sector perspective much of this growth was driven by the retail vertical. Its mobile share increased by 6% on average comparing 2022 to 2023.

Desktop remains the device of choice for higher value purchases however, with shoppers spending over €31 more on average compared to mobile.

As in-app experiences continually improve for shoppers, we expect mobile to solidify its position as the core device across Black Friday. This will be especially prevalent amongst Gen Z who overwhelmingly use mobile phones as their primary device to shop – 74% of those surveyed by Hubspot stated so.

3. Mobile’s rise mirrors that of influencers

Given the rise in mobile transactions it will come as no surprise that influencers also played a major role across the Cyber period as we predicted last month. Given the propensity of these partners to drive traffic from mobile app-based platforms, their growth as a reliable source of affiliate activity mirrors the growth in mobile sales.

Awin has seen a massive influx of new influencers joining the platform ever since the launch of its dedicated express sign-up solution. More than 10,000 new influencers have joined Awin thanks to the simplified process.

And these new partners duly grew their share of sales across the global platform compared to previous years, now accounting for 8% of total global sales over the Cyber period.

While influencers have been a core part of affiliate strategy in sectors such as fashion and health & beauty, verticals such as DIY and FMCG are seeing strong growth from them too as advertisers look to harness their audience engagement to generate sales outside of more orthodox affiliate types.

4. Brands adopting tech partners see AOV gains

Technology partners, which include a range of solutions from conversion specialists through to shoppable content, have set record performance over this year’s Cyber Weekend. Clicks were up almost 95% annually as Awin has seen more and more advertisers take advantage of the cutting-edge ecommerce tech available via the affiliate channel.

Collectively, these partners generated over 30% additional revenue for brands deploying them compared to last year, and AOVs increased significantly from €111 to €124. This was largely due to tech partners’ success in driving high ticket conversions within sectors such as electronics, white goods and the hotels & accommodation space where basket values frequently reach four-figures.

These partners’ ability to intelligently upsell and cross-sell to shoppers in sectors where there are often multiple elements to the product or service being bought no doubt helped advertisers maximise the value of the transactions they saw. An additional €13 in revenue was generated on average per sale. And with tech partners seeing an 18% increase in overall sales annually, it’s clear these partners are another useful addition for marketers to strategically use at this all-important time.

5. Electronics sector sparks to life thanks to steep discounts

Non-essential goods tend to see a decrease in interest during a tougher economy as shoppers reprioritise their spending. Despite this, the electronics sector generated an additional €6.3m in revenue this Black Friday compared to last year with strong promotions, cashback rates and incentives tempting buyers. UK electronics giant Currys experienced enough demand on the day that their servers went down, requiring a queuing system to be implemented to manage the influx of shoppers.

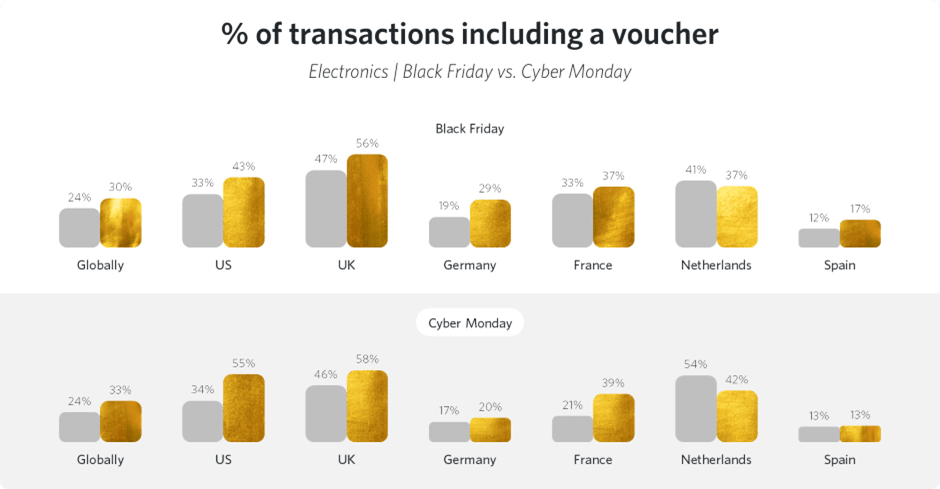

This was in part driven by forecasted heavy discounts for the industry and it appears consumers made the most of these offerings. The number of transactions in the sector including the use of a discount voucher on Black Friday increased annually by over 5%.

2023’s Cyber Monday saw that figure jump further again, with well over a third of transactions featuring the use of a discount voucher – up by 9% from 2022.

6. Black Friday offers continue to extend ever earlier

This Black Friday, we saw advertisers once again drive their offers earlier and earlier into the month, with some starting as early as October. This was to be expected given previous years’ trends. Online retail trade group IMRG suggested more than three-quarters of advertisers would go live with their offers on exactly the same day as 2022 and another 6% opting to launch them even earlier.

Network data also supports this wider trend when we looked at when the number of sales occurring with discount vouchers started to significantly grow.

Looking ten days prior to Black Friday, 23% of transactions in 2022 included a voucher, increasing to 25% in 2023. Furthermore, taking a deeper look at November as a whole, we see voucher code rates start to increase as early as three weeks away from Black Friday – last year saw over a fifth of sales converting with a voucher at 21% whereas as 2023’s rate increased to almost 24%.

7. Singles’ Day slowdown

Despite its status in the East, Singles’ Day performance was muted this Cyber period compared to previous years. Across the network, performance was down more than 4% from 2022, while a comparison to 2021 showed a significant decrease of almost 24%.

From a sector perspective, health & beauty continued to be the best performing category despite a 16% decrease in sales YoY illustrating its established popularity during Singles’ Day.

Voucher code usage also suffered a hit with 53% of sales converting with a code applied compared to 2022’s 58%.

A few factors are likely responsible for this year’s lower performance. Wary of the demand for discounts around the Cyber Weekend, many retailers appear to have kept their powder dry for the main event. In addition, many luxury brands in the West, popular with affluent Asian shoppers who drive a significant share of the day’s revenue, chose not to participate in Singles’ Day promotions in an effort to maintain brand image and distance themselves from more discount-led campaigns.

8. Shoppers were hungry for discounts, but some sectors held firm

Deep discounting is clearly a strong motivator for consumers, with a whitepaper published by YouGov stating 41% of surveyed shoppers were willing to wait for sale periods to purchase planned items. But has distrust in pricing strategies hampered consumer appetite for voucher codes and discounts?

Research undertaken by UK consumer advice company Which? found that on average, only 2% of items in the Black Friday sales were actually cheaper than at any point earlier in the year. This is indicative of the scepticism that’s been levelled against the Cyber period by consumers, who have questioned whether they’re truly finding a landmark deal or not.

Awin data suggests that shoppers were still hungrily seeking out promotions though.

Over Black Friday in the retail sector, the rate of transactions with a code rose from 33% to 36% annually. A third of global electronics sales this year included a voucher, an increase from 2022’s 28% while the fashion industry remained stable at a rate of 27%. Department stores, an industry that has been struggling amidst the recent economic pressures sought to also entice consumers into spending by increasing their discount use, jumping from 6% to 15% in 2023.

This wasn’t the case across all industries however. The telecoms and travel sectors saw a lower rate of voucher code sales compared to last year. On average telecoms voucher usage dropped from 15% to 13% across Cyber. But that doesn’t mean these advertisers didn’t offer promotions. Diving deeper diving into the mobile contract industry revealed cashback publishers saw a 22% growth in sales across the weekend.

Meanwhile, travel saw a reduction of discount usage from 28% to 21%. But, with January’s travel peak just around the corner, it remains to be seen whether these brands are holding out for what promises to be a strong year for them as demand for holidays floods back into the market.

9. Europe’s shoppers hold out for deals beyond Black Friday

Though Black Friday remains the biggest day for sales still across Europe, unlike its US counterpart where Cyber Monday is king for online shopping, shoppers were clearly keen to see if they could get a better deal across the weekend.

Looking at the share of sales across the four days in Europe, Black Friday’s contribution dropped from 35% in 2022 to 33% in 2023, with sales mainly redistributed to Saturday and Sunday as well as a slight bump on Cyber Monday.

While the sales split across the four days remained static in the US, the trend suggests European shoppers were more inclined to hold off from immediately purchasing their goods and instead open to waiting to see whether better prices would emerge later.

Similarly, Klarna found that European online consumers tended to be more price-conscious compared to American shoppers. 83% of those surveyed in the UK, 82% in Germany and 78% in the Netherlands stated the main reason they preferred to shop online was to compare prices.

And that was something Awin saw reflected in the types of partners being used to discover and buy products online in Europe. Comparison Shopping Service (CSS) partners saw their share of sales grow from 6% to 10% in 2023 as consumers increased used Google’s shopping tools to compare prices and find the best possible deal for their money.

10. BNPL publisher model flourishes across Europe and the US

Much has been made of the rise in use of Buy-Now-Pay-Later providers in recent years as many individuals have found it harder than ever to afford the things they want to purchase.

Inevitably, many industry figures were eager to see how the use of BNPL would play out against the backdrop of the Cyber Weekend when there would be a flurry of online shopping activity.

Adobe reported that BNPL usage had risen by a significant 72% compared to 2022’s same period, indicating the clear demand from shoppers for the payment option.

Of course, many of these BNPL solutions have become affiliates themselves, establishing their own member bases and audiences who have turned to them not just for their flexible credit options but also exclusive brand deals and promotions.

The increased demand for their payment support went hand-in-hand with the appetite for the deals they served up over the weekend. Globally, BNPL publishers on Awin generated an additional 42% in revenue compared to 2022.

From a regional perspective, the markets that witnessed the biggest growth in this space were the UK, Germany and Italy in Europe – these three markets made up 60% of all BNPL sales over Cyber 2023.

By contrast, the US made up a much smaller share – just 19% of all BNPL sales over the weekend. However, those partners still drove an impressive 42% growth in sales compared to 2022’s figures, not far behind the 54% growth that Europe’s BNPL partners witnessed.