Insight of the Month: CSS comes to retail’s rescue

Written by Alfie Staples on 5 minute read

The latest piece in our monthly series brings the spotlight on retail, where CSS is providing a bright spark amid a challenging climate.

Retail has endured a tough time of late. Fresh off the back of a mixed reception for Christmas, where reports of UK households dialling back on non-food purchases were contrasted with news of record holiday spending in the US, the ongoing economic tumult has left many retail sub-industries wondering if 2024 is a time to survive or thrive.

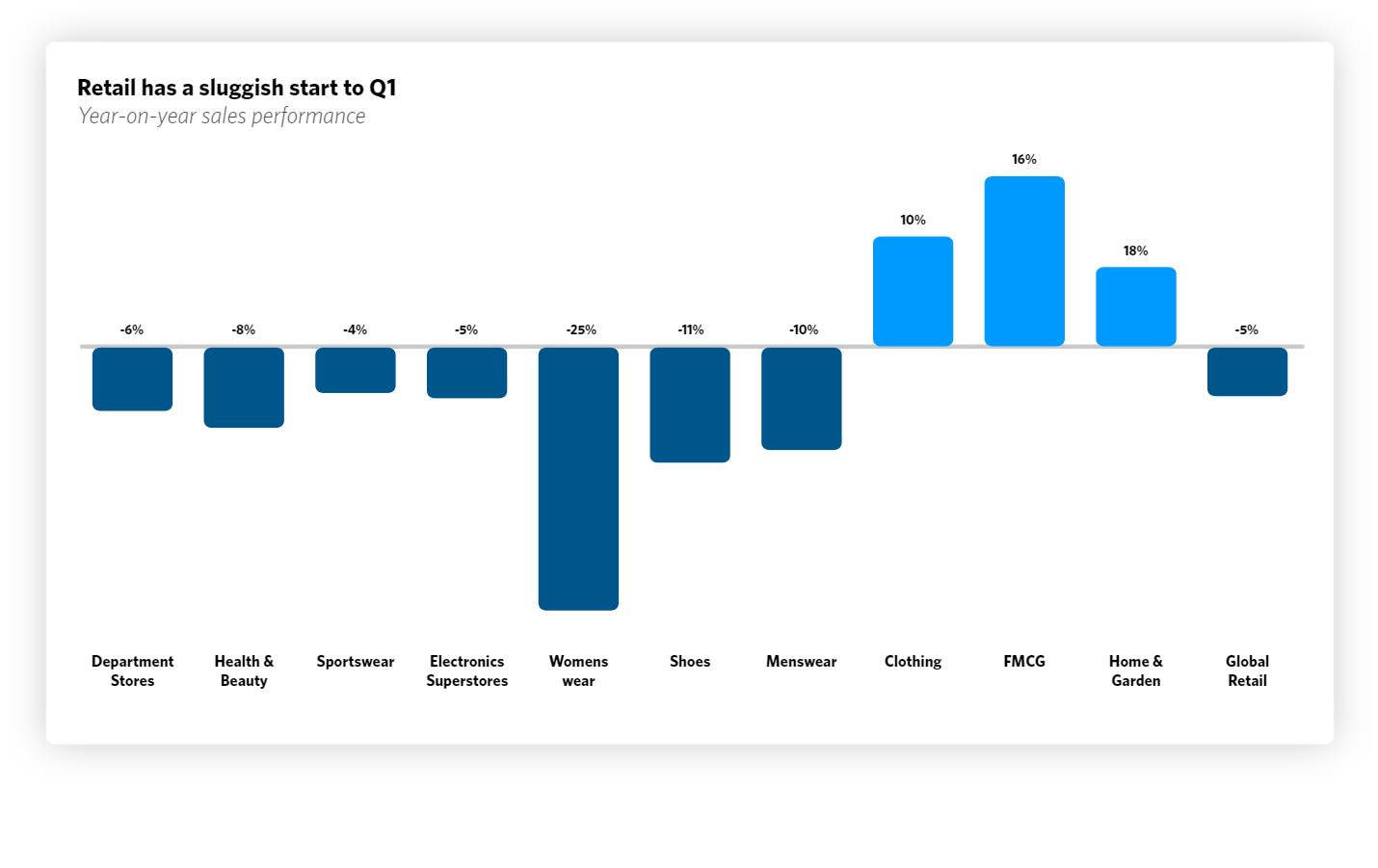

Looking at Q1, it seems any festive boost has failed to carry over into the new year. Retail sales dipped 5% year-on-year across the Awin platform, with fashion-related sub-industries like Womenswear (-25%), Menswear (-10%), and Shoes (-11%) seeing the biggest declines.

Given the +12% increase in Travel sales and a +2% increase for Telco over the same period, there is a sense that Retail is suffering more than most.

It’s not all doom and gloom, however. Sales are up for Clothing (+10%) and Home & Garden (+8%) — the latter now coming into its seasonal window. There’s even a +16% uptick for FMCG (fast-moving consumer goods), potentially driven by the continued appetite for pet food, snacks, and dairy products, which enjoyed a strong 2023.

When sales in a particular industry slow down, publishers often feel the bite. For the most part, they did, with one major exception.

Retail sales driven by comparison shopping services, aka CSS, bucked the trend by growing +16% year on year in Q1 2024. This is in stark contrast to the declines seen across many historically popular Retail publisher types, like Discount & Voucher (-14%), Cashback (-7%), and Sub-Networks (-16%).

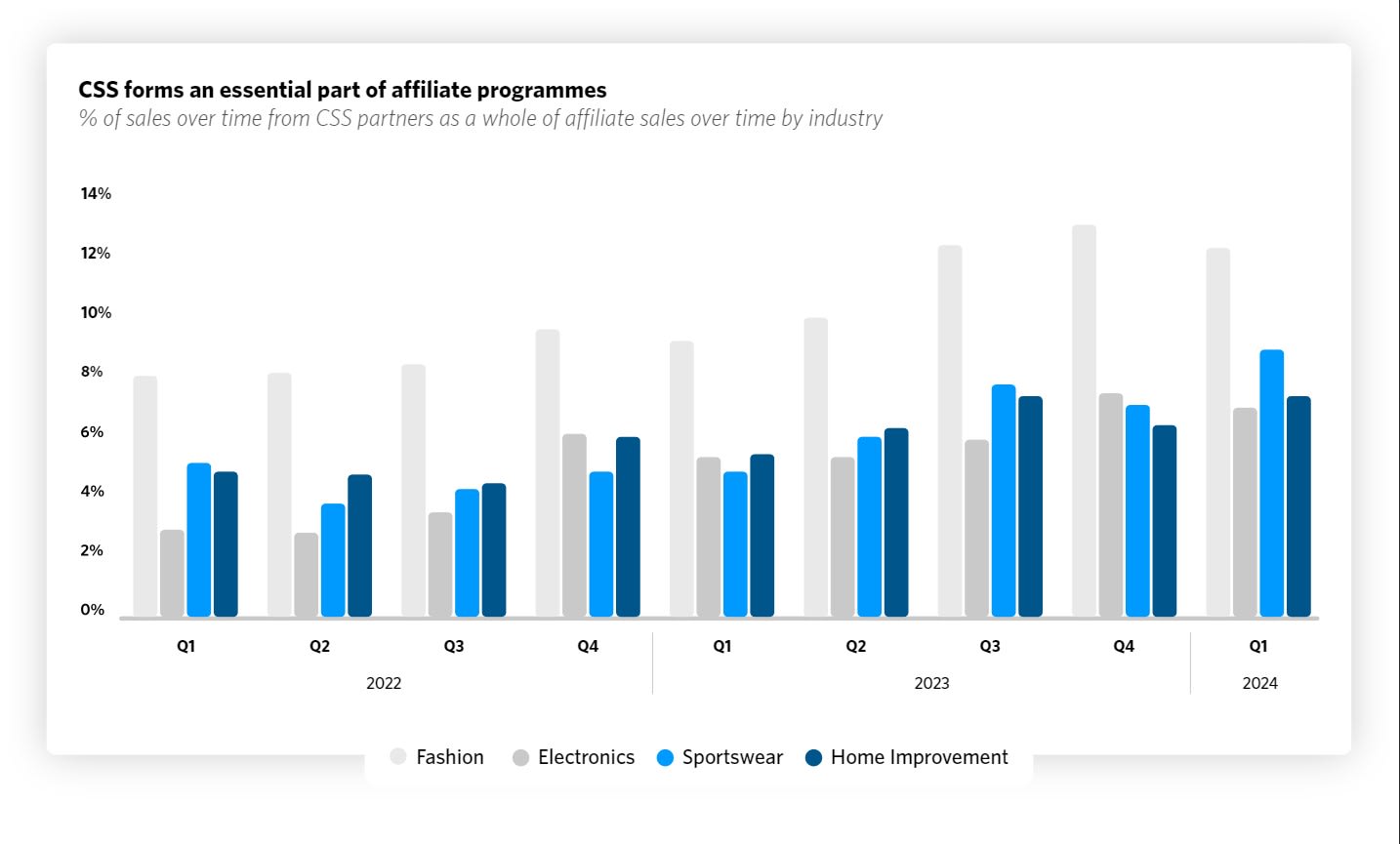

CSS now forms an essential part of retail affiliate programmes

CSS partners are largely recognised for their ability to power tactical acquisition and brand awareness efforts by optimising your Google Shopping ad space.

Despite their hugging of industry headlines, CSS’s growth is by no means confined to Q1 2024. The percentage of sales driven by CSS is up +29% across Fashion, +27% for Electronics, +59% for Home Improvement, and +30% for Sportswear over the past year.

Going back even further by comparing Q1 2024 with Q1 2022, CSS’s publisher market share has risen by +77%, meaning these partners now account for 8% of all sales on the Awin platform.

What’s more impressive is that these figures are essentially being driven by the model’s popularity in a single region.

CSS took flight in 2017 with the introduction of Google’s Comparison Shopping Service partner program via a well-publicised €2.4bn fine from the EU for stifling competition. This essentially repositioned Google Shopping as an independent business that comparison sites can leverage to promote retailers’ products.

The impact of tighter scrutiny on Google Shopping in Europe is highlighted by CSS’s virtually non-existent presence in the US, where a lack of restrictions has maintained the search giant’s monopoly. Just 0.2% of CSS sales on the Awin platform derive from the US, while the UK (48%) and fellow European players Germany (16%), Spain (11%), the Netherlands (6%), and Italy (5%) eat up virtually all of the remainder.

Interestingly, there seems to be more chance of a further twist in the tale across Europe than the levelling of playing fields in the US. Only last month, a Polish court ordered Google to remove Shopping from its country’s search results altogether due to the advantage it holds over local alternatives like Ceneo.pl.

Though it seems unlikely that Google would be forced to axe such a popular feature across Europe, it shows that many still feel the current system works in the search giant’s favour. For the CSS partners that are finding success in 2024, wider support for the Polish ruling could prove catastrophic.

Why is CSS proving so popular?

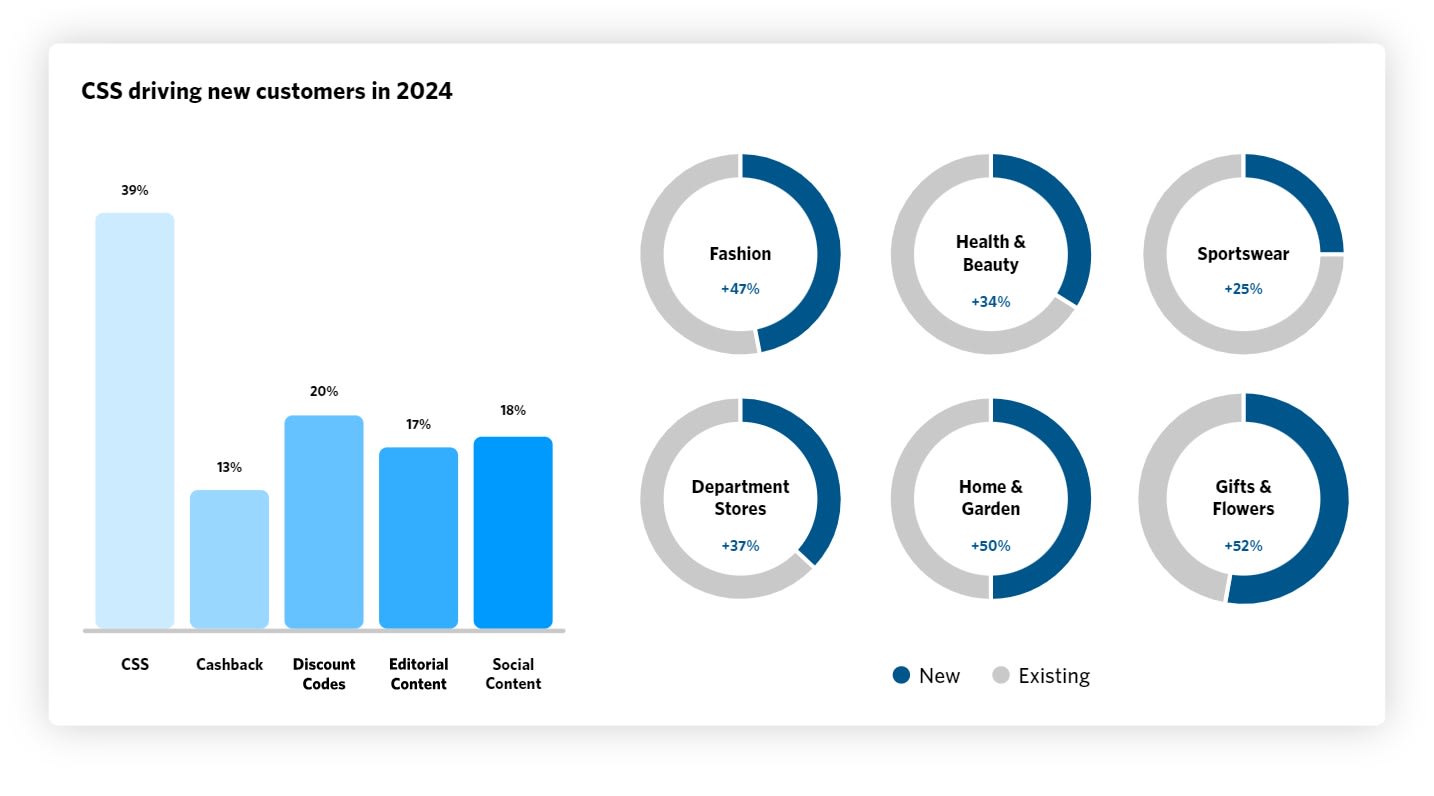

CSS partners are rightly positioned as vehicles for brand awareness, but they’re perhaps best celebrated for their ability to acquire new customers.

An impressive 39% of Retail customers driven by CSS are new, with traditional acquisition channels like Social Content (18%) and Editorial Content (17%) barely reaching half of this total.

In Gifts & Flowers, the percentage of new customers driven by CSS goes as high as 52%, with Fashion not far behind on 47%. Even in places with much lower new customer weightings, like Sportswear on 25%, there is no publisher type that gets close to CSS.

CSS has a lot of momentum on its side. In fact, the only caveat is a very logical one.

In a space that revolves around bidding for consumer interest on one of the most popular product discovery tools, high competition justifiably produces lower returns compared to other publisher types. CSS’s return on investment of 14:1 is better than Content & Creators (13:1), but significantly lower than Discount & Voucher (22:1), Loyalty (17:1), and Cashback (16:1).

Nevertheless, as we monitor the progress of a new cornerstone of retail affiliate marketing, it will be interesting to see just how far CSS’s growth can go.

Interested in discovering more about CSS partners? Check out our recent roundup of the top 10 CSS partners on the Awin platform.